Intellectual bankruptcy in the gas price debate

Record-high gas prices have elicited a record-high supply of silly solutions

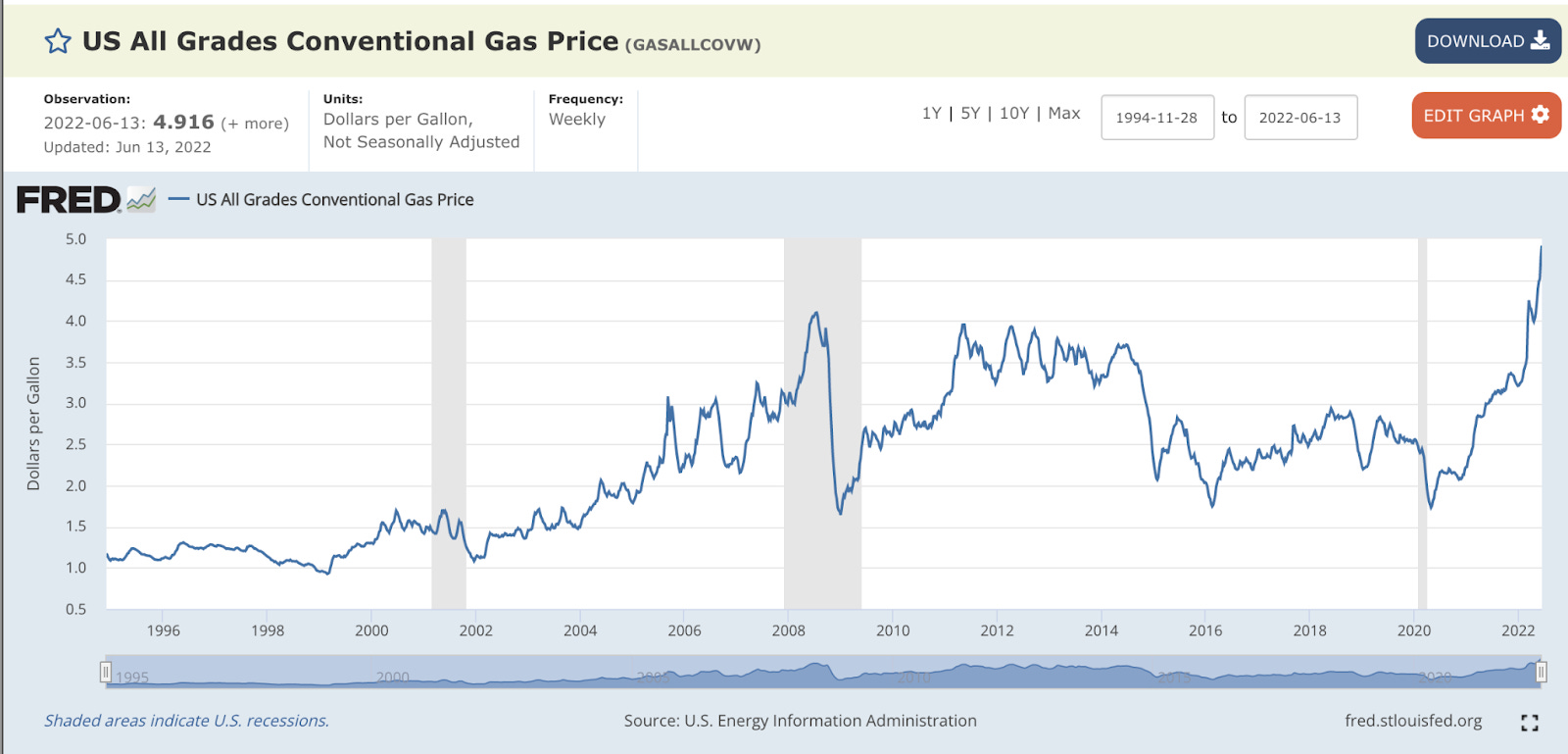

Gas prices have recently recently to all time highs, contributing to some of the largest headline inflation prints in forty years.

Naturally, these prices are an economic disaster. Gas consumption is famously price-inelastic in the short-run, meaning that it’s rather difficult for consumers to immediately transition away from gas usage in response to higher prices. As a result, the recent spike in gas prices has caused an immediate immiseration of millions of consumers who now have to cough up hundreds of dollars more per year for their daily commutes.

Less importantly, gas prices are a major political problem. Despite the fact that political leadership has relatively little impact over the price of a gallon of gasoline, gas prices are far more salient to consumers than other prices (it probably doesn’t help that gas prices are broadcast on huge signs on every major road). Unsurprisingly, there is some evidence that gas prices have a negative correlation with presidential approval ratings. Consequently, the Democrats are under great pressure to try to deliver relief at the gas pump.

Unfortunately, the proposed solutions are all terrible and far more likely to exacerbate the crisis than solve it.

The origins of the crisis

Before delving into the “solutions”, it’s worth taking a step back and exploring how we got where we are. Why are gas prices so high?

Most obviously, there’s the war in Ukraine. Russia is the world’s third-largest producer of oil, composing 11% of the global supply (after the US’s 20% and Saudi Arabia’s 11%). In response to the invasion, Europe and the US imposed sanctions on Russia and oil imports cratered. It’s worth flagging that Europe has not prohibited importing oil from Russia (yet—they say they plan to ban Russian oil imports by year’s end), but the broader financial sanctions and reputational consequences of dealing with Russian entities has strongly discouraged imports in the meantime. When the same amount of demand is faced with a lesser supply, the price of crude oil naturally rises. And since the price of crude oil is by far the largest input into gasoline, it’s unsurprising that the price of gas has increased correspondingly.

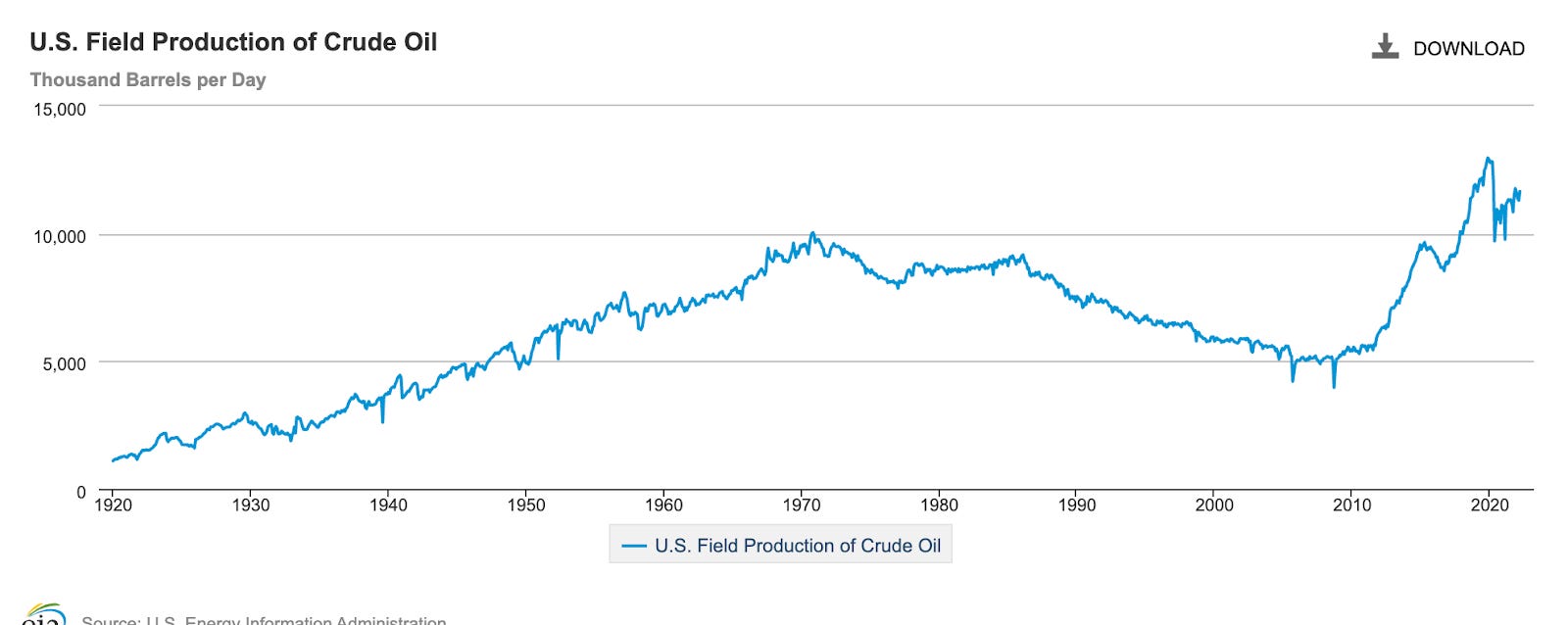

However, the natural response to higher prices is for other producers to up their production. Imagine you have a shale rig trying to access difficult-to-extract oil. In a low price environment, there’s no way for you to make your money. bank But if prices are sky-high, now it might be profitable. So we should expect that other producers—maybe those operating in marginal oil basins—should step in to fill the void left by Russian producers. It shouldn’t completely replace them (if they substituted Russian oil one-for-one and pushing the gas price back to where it was before, then the new suppliers would have no economic incentive to remain in the market), but it should get us at least closer.

Unfortunately, it’s not so easy to expand supply. Oil extraction is highly complicated, and acquiring the equipment, manpower and business relationships to quickly get the oil back on market is rather difficult. But it’s possible! But the issue is risk. The shale oil boom has allowed the US to more than double its oil production between 2010 and 2020 as companies rushed into the space to take advantage of the new technology.

But a lot of those companies got completely burned when prices collapsed in 2015, when prices fell by more than 50%, and 2020 (when prices collapsed by half again).

With all this history, a lot of firms are highly reluctant to jump back into the fray. Suppose you’re Exxon Mobil and you spend $1 billion to bring new oil production online. It takes a few months to hire the extra workers and get the site up and running. You start selling oil and are making a pretty penny, but then Russia and Ukraine sign a treaty ending the war and the oil price falls by 50%. You can’t recoup any of the upfront costs you just spent! The history of over-investment leading to price busts has induced a lot of financiers to insist that the oil companies they’ve supported return profits back to shareholders in the form of dividends, instead of reinvesting it in production.

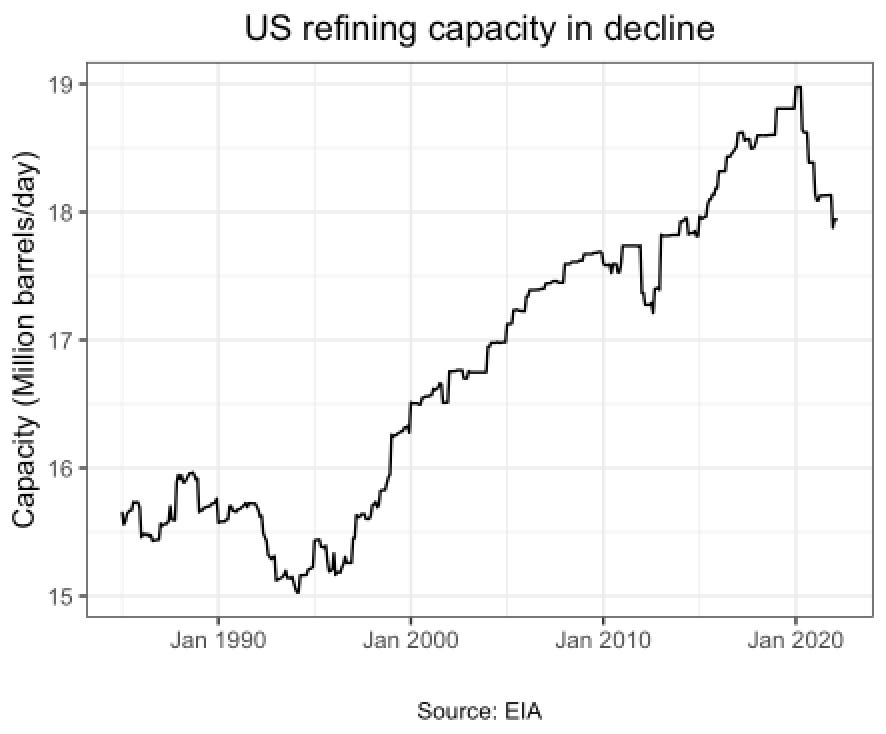

The final relevant feature is the collapse in US refining capacity. Before oil can become gasoline, it needs to be processed. Refineries are highly expensive pieces of capital expenditures, and no reasonable oil company could justify building a new refinery for what may be a temporary increase in prices. When many refineries shut down during the COVID-19 era price crash, it has been difficult to convince many to restore their activity. As a result, oil refinery capacity in the US has fallen from 19 million barrels/day in January 2020 to under 18 million barrels/day today.

The “solutions” to the problem are worse than nothing at all

Considering this backdrop, what have the politicians in power actually proposed?

Demand subsidization

The simplest idea is to just send consumers money to afford gas. The Biden administration claims that it might make a decision by July 4 whether or not to create a gas tax holiday (though Kalshi traders seem to think there’s only a 22% chance it actually happens). Mainstream media outlets have reported that the Biden administration was previously mulling sending people gas rebate cards, though the idea has largely been mothballed after it became clear that you can’t actually restrict spending just to gasoline (money is somewhat fungible). State-level politicians like California governor Gavin Newsom, New York governor Kathy Hochul, and Pennsylvania gubernatorial hopeful Josh Shapiro have all proposed some form of gas rebate.

All of these ideas would make the situation worse. At the risk of sounding like an Econ 101 hack, subsidizing demand increases prices. If supply does not meaningfully increase in the short-run (which is a fair assumption) and gas prices are fairly flexible (another fair assumption), increasing demand will translate nearly one-to-one into higher prices. The bill just becomes a transfer from state or federal coffers into the pockets of oil companies.

We do subsidize demand in other domains with reasonable success, like food stamps or rental vouchers. But there are two clear differences. First, particularly with food, production adapts. If people have more money to buy food, prices go up so farmers grow more food and prices largely fall back down. But if that last step is missing, then all you get is “prices go up”. Second, they’re targeted towards a specific subpopulation. So for housing, where supply is artificially constrained by a byzantine maze of zoning and land use regulations, rental vouchers probably do push up the price of housing, but since that price increase is spread across the entire population, the price increase for the voucher recipients is far smaller than the size of the voucher. As a result, it’s a redistribution from the general population towards the poor and, to a lesser extent, landlords. But without a supply response, a general demand subsidy will just increase prices.

Anti-gouging laws

The second big idea is to pass new anti-gouging laws. Back in May, the House of Representatives passed the Consumer Fuel Price Gouging Prevention Act. The bill–which passed with zero Republican votes and faces near certain death in the Senate–would enable the President to declare an “energy emergency” whereupon “unconscionably excessive” price hikes would become illegal, while empowering the FTC to investigate such price increases.

The idea seems to imagine that the cause of gas price inflation is the greed of oil companies. Oil companies certainly are greedy, but the explanation is wanting. When gas prices fell 50% in 2015, did oil companies get 50% less greedy? No, the greed is a constant: oil and gas companies will always try to seek the profit-maximizing price level for a gallon of gas. The loss of supply from Russia simply raised that profit-maximizing price level.

Even if greed didn’t cause the price hike, why would it actually make it worse? There are two major reasons:

First, price caps cause shortages, much like in the 1970s. The current price roughly hovers around $5.00/gallon, with some states like California having prices top $6.30. That price signal means that there are enough people in California willing to pay at least $6.30/gallon such that gas companies can clear out their inventory at such a price point. If a gas station raises prices above that level, people will flock to their competitors. If they lower prices, then people will come from their competitors towards them to take advantage of the savings.

But if they’re selling out at $6.30, what happens if the government were to mandate prices cap out at $5.00? Well, then people would want to buy a lot more gas, and then the demand would exceed the amount actually supplied, a.k.a. Shortages. This is the exact situation that occurred in the 1970s when the Nixon administration imposed price controls, and people waited in lines for hours to purchase oil. High prices at the pump are certainly unfortunate, but legislators can’t just waive a magic wand and order prices to be lower without causing even worse consequences.

Second, it discourages a supply response in the long-run. Suppose an oil company is trying to decide whether to invest in a new rig. Obviously, they need to make price projections: if prices fall too low, they risk losing money. But there’s a chance that prices could rise, at which point they’ll make a fortune. If they know that there’s a limit to how much money they can make in the best case scenario, the equilibrium level of production will be lower. As a result, Congress would be robbing Peter to pay Paul. They may get lower prices now, but at the price of higher costs in the future.

The “windfall tax” idea has the same downsides. By saying that oil companies can’t make as much profit in the long-run, it discourages oil companies from building as much capacity in the short-run. They’ll have a smaller disincentive effect than price controls, but they’re also highly unlikely to have any meaningful effect on prices. There’s a clever infra-marginal gas tax idea that I won’t discuss at length since this piece is already overlong, but the main reason why it evades the downsides is because it doesn’t actually directly lower gas prices (instead it uses the revenue to finance ideas, discussed below, that actually might work).

Rate hikes

The final idea is to hike interest rates. I discussed this in my last post, but the tl;dr goes something like this:

The Fed has a dual mandate to manage inflation and full employment

Inflation has been skyrocketing, so the Fed is under enormous pressure to reduce it

A lot of that inflation has been gas prices (a supply shock), which as we discussed, isn’t really something the Fed can affect very much. As a result, the Fed is supposed to be targeting “core” inflation that ignores food and energy prices

But due to political pressure, the Fed seems to be stealth-targeting “headline” inflation (which includes those measures)

So how could rate hikes lower gas prices? By destroying demand. If you cause wide-spread unemployment and people have less money, they will have less money to spend on gas. An adverse supply-shock combined with an adverse demand shock might get prices back to where they were before, but at a terrible price (in the long-run, a higher interest rate environment also risks discouraging investment since the present costs of financing a new refinery or rig rise relative to the future benefits of revenues from that refinery or rig, but that’s not that germane to the current discussion). On balance, it seems like a highly inappropriate solution to the problem.

What actually might work

At some level, the problem is fairly thorny since the ultimate cause (the Ukraine war) is not something that can just be solved by an act of Congress. But there are some steps that could materially improve the situation.

As Arnab Datta and Skanda Armanath of Employ America have previously written, the Biden administration could direct the Strategic Petroleum Reserve to sell “put options” on oil to create a soft floor on prices. In short, they’d sell oil out of the reserve today, in exchange for a guarantee to purchase oil in the future at a given strike price. Suppose that strike was $70: since the SPR is functionally agreeing to buying large amounts of oil at that price in the future, that offers a floor on how low oil prices could go. That could reassure skittish investors that their investments in expanding supply won’t be in vain by removing concerns of a price crash. Incidentally, such a policy also has the clever feature of discouraging oil consumption in the long-run (a price floor on oil is like a stealthy carbon tax in a low oil price environment), which could assuage the concerns of environmentalists who are uneasy about the idea of aggressively promoting fossil fuel production.

The rest of Datta and Armanath’s article contains several other clever ideas that really do seem promising. They suggest using the Treasury’s Economic Stabilization Fund to offer solve financing issues to enable refineries to expand production, and using the Defense Production Act and other measures to address bottlenecks in oil production, like shale sand to steel pipes. I recommend checking it out in full, because it represents the best set of solutions I’ve read to date. Sadly, the ideas that have actually caught on are intellectually lazy, falling for the simplicity of “just give people money” and “blame big corporations”. A more sober-minded solution set is far less sexy, but actually could help address the issue.