Six underrated features of the student debt forgiveness debate

Before going further, we’d quickly like to remind you that if you’re enjoying the contents of the newsletter, please consider subscribing and sharing!

Now back to the action…

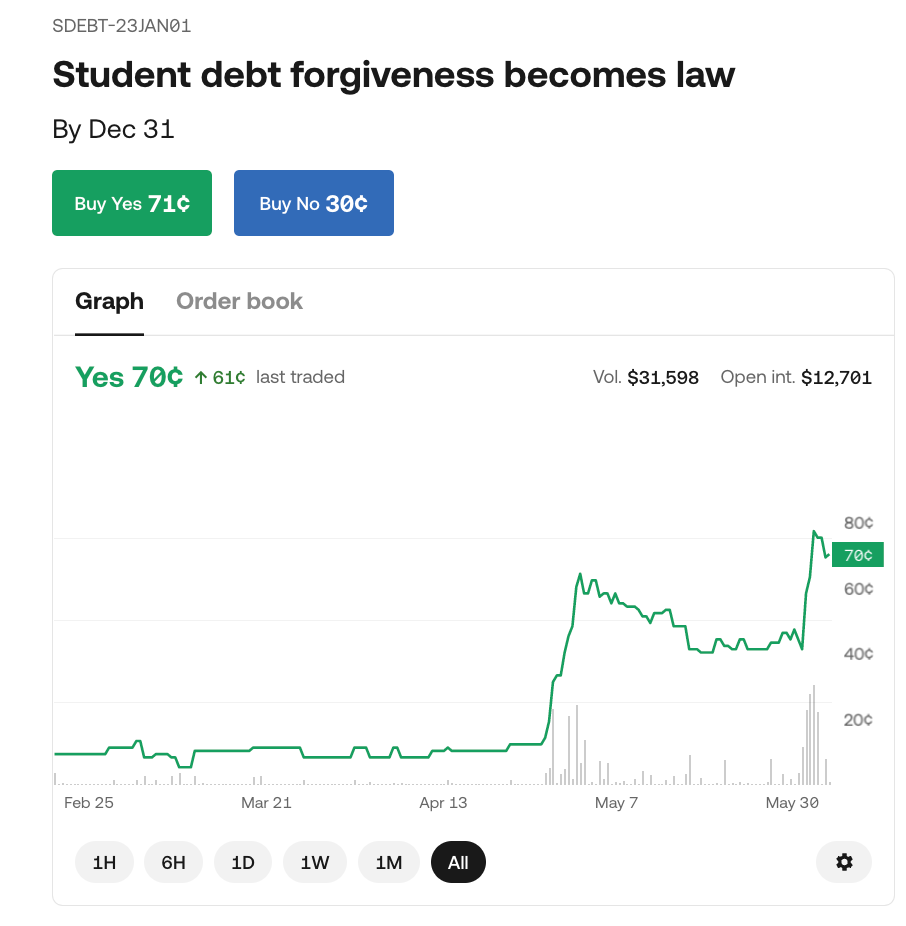

President Biden recently made headlines after reports have emerged that his administration is mulling forgiving up to $10,000 in student loans for borrowers making under $125,000 a year. Prediction markets seem to think these claims are credible, and estimate the odds of a broad-based student loan forgiveness event this year at roughly 70%.

The move has predictably sparked a firestorm online. Many critics allege that the move arbitrarily rewards the relatively well-off, without assisting those who never attended college at all. Other critics, often on the left, allege that the $10,000 sum is insultingly low and will hardly help those with the greatest need. It has further kicked off a debate about whether college-educated urbanites have too much sway in the Democratic Party (I’d recommend this great article from Jerusalem Demsas in The Atlantic on the subject).

I don’t particularly want to wade into the debate about the propriety of forgiveness. Instead I just want to share what I think are some underrated features of the discussion at hand that may be helpful in guiding one’s opinion.

Don’t focus on the eye-popping sums

Advocates of forgiveness often highlight graduates with six-figure debt loads who struggle to pay back their loans. Fortunately, this narrative is highly misleading. Average debt per borrower is around $25,000 and 78% of those at public four-year institutions have debts under $30,000.

So where are all the crazy numbers of $200,000 debt numbers coming from? Some of it certainly comes from those who attend non-selection private institutions, as student aid at in-state public schools is typically far more generous. But the biggest culprit is graduate school. The average student loan debt of a graduate student is $73,000, including over $150,000 for law students and $250,000 for medical students. Indeed, according to data from the College Board, 47% of all federal student loans went to graduate students in the 2020-21 school year, up from 32% in 2005-06.

That’s not to say that graduate students are irrelevant, but considering how average earnings for those with tertiary degrees (especially doctors and lawyers) are so enormous, they are probably not the group most in need of assistance. Indeed, default rates among graduate students are far lower than among undergraduates. There’s a world of difference between a doctor with $250,000 in student loans but will soon pull in $200,000/year, and a college dropout with $20,000 in debt but expected income of $45,000/year.

Defaults tend to concentrate among those with loan debt balances

Because of that earnings differential, those with the largest loan balances are among the least likely to struggle to repay their debt. Per data from the Federal Reserve Bank of New York from the 2009 cohort, about 1/3rd of borrowers with loan balances between $1,000 and $5,000 defaulted by the end of 2014, compared to 20% of those with balances above $25,000.

Source: Federal Reserve Bank of New York

How could this be so? At some point, those with the largest debts are just because they went to elite schools or possess a medical or law degree. They have large amounts of debt, but can (relatively) easily pay them off. But at the lower debt balances, the main takeaway is that many of these borrowers (1) never finished their degree, and (2) have either no job or a job with very low incomes. It isn’t that they cannot repay the amount of student debt that they have, it’s that they cannot repay any student debt. It’s worth flagging that getting exact data on these shares is difficult–default data often comes from Federal Reserve Bank of New York Consumer Credit Panel data (via a partnership with Equifax) which does not have degree completion data.

How does this impact the student loan debate? It does suggest that a capped student forgiveness plan (e.g. Biden’s $10,000 plan) could have disproportionately large benefits for those most distressed, while the larger plans proposed by Elizabeth Warren and others might be focusing on the wrong crowd. But it nevertheless begs the question that perhaps the forgiveness debate is focused on the wrong target: the issue may not be large debt amounts, it’s the low wages and low graduation rates.

In fact, if extreme distress is the main enemy, existing tools like income-driven repayment (IDR) plans can help a lot. Under an IDR, former students pay a share of their income to repay their debt. If you’re unemployed, you pay nothing. If you make little, you pay little. Data from the Federal Reserve Bank of Richmond suggests that these IDR plans can majorly reduce default risk. The fact that only 27% of borrowers have enrolled in these plans suggests that there may be large room for improvement on the default front without actually touching forgiveness.

The student debt crisis is a child of the Great Recession

One positive feature of the student debt crisis is that many of its worst effects may be easing. Back during the 2008 financial meltdown, the terrible jobs market meant a lot more people went back to school, but the lower family incomes meant that they had to borrow a lot more money to do so. That some states cut back on state education funding due to budget shortfalls may have also contributed to the increase in debt during this period.

The data bears this out. Total number of student loan borrowers nearly doubles from 2000 to 2011 before falling by about 33% by 2020, according to data from the College Board. Meanwhile, average debt per borrower spiked more than 11% (inflation-adjusted) during the recession. Overall, total student loan debt incurred per year more than doubles from 2000 to 2011 before swiftly falling off.

Source: College Board

Does this mean that student loan debt doesn’t matter anymore? Of course not. People who incurred debt during that period still have to pay it off and may struggle to do so. But it’s worth flagging that macroeconomic conditions play a large role in the student debt situation.

Debt overhang is severe problem for distressed borrowers

Debt forgiveness could help borrowers through two principal channels: a cash-flow channel (borrowers who were formerly paying $300/month now can use that $300 for any other needs they have) and a wealth effect (no more liability on their balance sheet). For highly distressed borrowers who are currently not repaying their debt, the second effect can be highly significant.

One study by economists Marco Di Maggio, Ankit Kalda and Vincent Yao exploits a fantastic natural experiment to estimate just how large the impact of forgiveness could be. One loan servicing company lost paperwork for thousands of delinquent borrowers, which allowed them to compare delinquent borrowers for whom the paperwork was lost (and thus their loans were thus randomly “forgiven”) from delinquent borrowers under the same company for whom the paperwork was retained. These groups are plausibly identical except for the random loan forgiveness. Likewise, because none of these borrowers were paying back their loans at the time, there is no direct cash-flow effect. Rather, all of the effects of random forgiveness stem from wealth effects. Average forgiveness size roughly $8,000 which, due to inflation since the event, maps pretty closely to the proposed $10,000 limit.

The results were fairly striking. Not only did the borrowers pay back substantial amounts of other debts (around $4,500) but their labor market outcomes improved dramatically as well. The hypothesis is that even though the borrowers were previously not repaying their student loan debt, they knew that if they took a better job that their wages would start being garnished. With the slate wiped clean, their rates of moving for work increased substantially and household income jumped around 10%.

This does not hold implications for the majority of borrowers who are not delinquent, for whom wage garnishment is not an operative concern. But it does suggest that targeted forgiveness at those who need it most isn’t just a “handout”, it could have large positive effects for recipients in the long-run as well.

The little details of implementation matter

One major flashpoint in the debate is about means-testing. Of course, all else being equal it seems silly to hand over large benefits to soon-to-be wealthy doctors from wealthy families. But the cost of administrating means-testing can often be highly onerous. For example, the best evidence suggests that the byzantine difficulties of filling out the FAFSA (the federal student loan eligibility form) discourages uptake, as 20% of eligible Pell Grant recipients did not re-file the FAFSA to continue receiving benefits the next year. Proving income eligibility often can be highly burdensome, and it’s worth considering whether the savings from excluding the wealthy are worth the time tax on those in need.

As a further illustration of “details matter”, it’s also worth considering the tax treatment. For now, student debt forgiveness is a taxable event. A poorly designed student loan forgiveness program could thus saddle borrowers with a major tax bill they are unable to pay. The Public Service Loan Forgiveness program and many others do not have this issue (though they have many other implementation issues that mean a lot of would-be eligible participants do not take advantage of the program), but it is an example of the way execution matters in program effectiveness.

The biggest effect will be in the long-run

Student loan forgiveness will not help people soon to enter college be able to afford it, only help those who have already incurred debt. If colleges anticipate student loan forgiveness in the future, there’s a risk that they may increase tuition (or decrease institutional aid) while implicitly promising borrowers, “don’t worry about all the debt, much of it will be forgiven anyways”.

There’s some evidence that federal programs do have this dynamic. One study from economists at the Federal Reserve Bank of New York found that federal subsidized student loan amounts increase tuition by “60 cents on the dollar” (i.e. a one dollar increase in federal students loans per person to an institution raises tuition per person by 60 cents, in part due to decreased financial aid given by the college itself). This is hardly the last empirical word, but it does suggest that a loan forgiveness program, without corresponding reforms to college pricing otherwise, may end up becoming a “robbing Peter to pay Paul” situation where future students have to eat the bill to pay for previous student loan forgiveness.

Conclusion

These takes aren’t meant to be dispositive. It seems clear to me that some borrowers will see large and enduring benefits from a well-designed forgiveness program with some pretty clear costs. That said, focusing on only the forgiveness component without addressing why college costs have grown so much seems to be an unfortunate byproduct of the fact that forgiveness (probably) can be executed by executive order whereas college reform plans require Congressional majorities. Spending billions on college attendees is an awkward fit for a highly inflationary environment, yet by our best estimates it is the world that will likely come to pass. Far be it from me to judge whether these costs are worth the benefits, but I hope the debate can go forward in a slightly more informed manner.