What is the Fed targeting?

Welcome readers old and new to the Prediction Markets newsletter!

The Federal Reserve Open Market Committee announced a 75 basis point hike in their June meeting. Before Monday, that would’ve been a major shock, but someone (probably at the FOMC) leaked to the Wall Street Journal that this was coming and markets reacted accordingly.

It’s worth flagging that the principal effect of this decision is not merely a 0.25% difference in the cost of borrowing. The main effect is to change expectations about the future growth in the money supply and credit conditions. Indeed, per Kalshi’s forecasts, the odds of 12+ hikes on the year jumped from 21% to 80%, and the odds of 13+ hikes jumped from 9% to 62%. These numbers roughly mirror what we see in other market-based forecasts, like CME’s fed funds futures. In short, this decision wasn’t merely “front-loading” hikes that would’ve occurred anyways–it was an act of tightening across the board.

The Fed seems to be ignoring their preferred measure

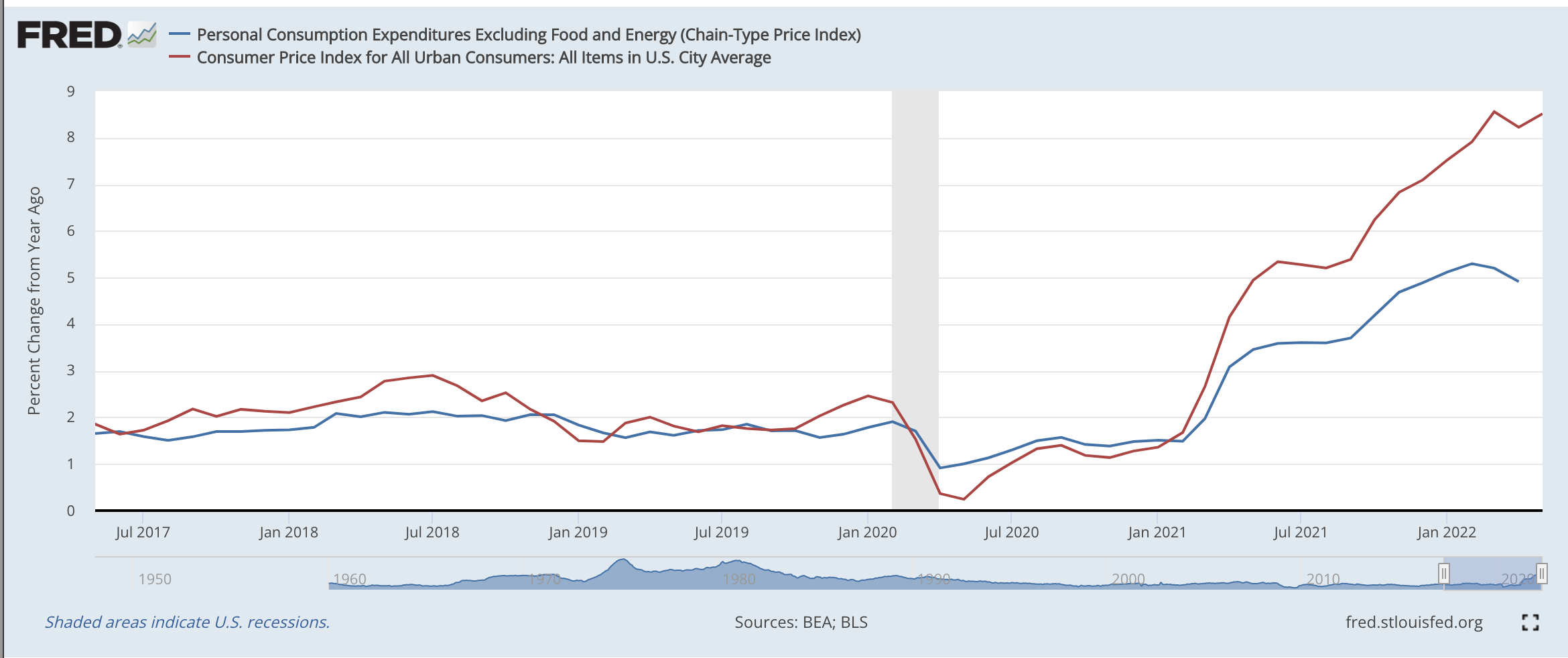

Fed chair Jerome Powell repeatedly mentioned during his speech that inflation “surprised” to the upside. That was the stated reason for why the Fed abandoned their intention of doing a 50 BP hike in favor of a more aggressive stance. But the Fed’s preferred measure of inflation–core personal consumption expenditures (PCE)–has remained flat at 0.3% the last few months. The eye popping numbers have largely come from headline consumer price index (CPI), a different measure.

Why do these two numbers tell such disparate stories? It helps to understand the difference between the two measures. To construct the Consumer Price Index, the Bureau of Labor Statistics surveys households in urban areas on the prices they pay for various goods and services. To construct PCE, the Bureau of Economic Analysis surveys businesses to determine the price of goods and services in all areas, not just urban areas. PCE also includes services outside the scope of CPI–such as employer-provided health care costs–and has different weights on different services. Because of its different (and better) treatment of substitution of goods, PCE tends to run slightly below CPI. However, it also takes longer to calculate: PCE normally comes out around three weeks after the CPI print.

But most importantly, headline CPI includes expenditures on food and energy, which core PCE does not. Food and energy prices are notoriously highly volatile, and are not generally predictive of future month gains. While food and energy obviously matter to household budgets, it’s important to exclude these categories when trying to project the future path of inflation.

Should they just target headline CPI?

So what’s going on here? It sounds like the Fed is targeting headline CPI. In fact, during the press conference, Powell hinted that the law requires the Fed to tackle all inflation, not just core inflation. And since people have to live with high food and energy prices, the Fed should incorporate that into their thinking.

That reasoning seems backwards to me. I’m no lawyer, but the Fed has always targeted core inflation without encountering legal issues so the “my hands are tied” argument seems weak. The “people experience high energy prices” is superficially true, but as Powell himself acknowledges earlier in the press conference, monetary policy is rather ineffective at targeting commodity price changes from adverse supply shocks. People also have to live with unemployment, so hiking rates in an ineffectual bid to combat sky-high gas prices seems rather counterproductive.

I think the most charitable interpretation is that the Fed is trying to manage inflation expectations. Since headline CPI is what’s reported in, well, the headlines, that would form the basis for most people’s expectations. If inflation expectations become unanchored, you might see people preemptively raising prices and wages in expectation of future price increases. Relatedly, people might start spending more now in expectation that the goods will be more expensive in the future, inducing even more price increases. That’s the dreaded inflationary expectations spiral.

But by the Fed’s own admission, inflation expectations remain well-anchored. 5-year, 5-year breakeven rates (the difference between inflation-protected Treasury bonds and unprotected bonds and represent market expectations of inflation 6-10 years from now) remain at 2.32%. The 5-year breakeven (years 1-5) is 2.88%, but a lot of that can be chalked up to elevated inflation in that first year, and suggests near 2% inflation for years 2-5. And is there any evidence that consumers are spending more in anticipation of price hikes? Consumer sentiment survey is pretty messy, but the best I can tell is that this evidence is lacking.

Why the Fed can’t target oil prices

I asserted previously that the Fed can’t really reduce volatile oil and gas prices. Despite inflation expectations largely being formed by gas prices (after all, they’re a huge part of households’ repeated purchases and their prices are broadcast on large signs on every major road), their hands really are tied.

Unlike e.g. hotel prices, gas prices are spiking from supply-side issues. The war in Russia has caused major disruptions to the global oil market. Oil production and refinement is hideously complicated and refineries and rigs can’t be just turned on at the snap of a finger. Moreover, shale producers are leery of rushing in to expand production during a time of high prices, only to get burned in case prices collapse.

Normally rate-hikes lower prices by reducing aggregate demand. To get gas prices back below where they were before the Ukraine war, you can’t just lower aggregate demand back to January levels. Even at the same level of aggregate demand, prices would be higher today because of the supply shock. That’s why most policy guides understand that monetary policy is rather ineffective when dealing with supply-side crises. If you wanted to lower gas prices that much, you’d have to put a lot of people out of work–a poorer country couldn’t afford to spend as much on gas and prices would fall. But that’s a terrible choice to make. The Fed targets core measures for a reason.

A better case for 75 BP

I’ve been pretty consistent here that a more aggressive hike schedule is entirely warranted for a simple reason: back when the market was pricing in a 50 BP hike schedule (and around 10-11 hikes on the year), nominal GDP expectations were well-above trend. Sadly, we don’t have a liquid NGDP futures market in this country so we can’t say for sure how NGDP futures have reacted to Wednesday’s announcement. But the Fed should just target the forecast. If market-based forecasts suggest current policy is failing to reach the target, we should just hike more/signal more aggressive policy until it does.

In my opinion, that’s the strongest case for the current policy. But the Fed is not making that argument. I’ve been somewhat sanguine about overall Fed policy, but one of my biggest frustrations is ambiguity about how they are making decisions. Despite numerous press conferences and speeches, the Fed continues to flip-flop between frameworks. They adopted a flexible average inflation target, then stealth-abandoned it (without admitting as much). They use core PCE as their preferred measure, but appear to have stealth-abandoned it as well. Considering how powerful forward guidance can be as a tool, it would be nice if the Fed was more predictable about how they make decisions. Guidance via WSJ leak is not a sustainable policy.